On the Margin Newsletter: Investors’ rotation into small caps isn’t just technical

blockworks.co 18 July 2024 22:19, UTC

blockworks.co 18 July 2024 22:19, UTC Today, enjoy the On the Margin newsletter on Blockworks.co. Tomorrow, get the news delivered directly to your inbox. Subscribe to the On the Margin newsletter.

Welcome to the On the Margin Newsletter, brought to you by Ben Strack, Casey Wagner and Felix Jauvin. Here’s what you’ll find in today’s edition:

- Investors are rotating into small cap value-tilted stocks. We unpack potential explanations.

- US spot ETH ETF issuers have set their planned fees. Let’s compare the numbers.

- The Trump campaign is raking in crypto donations from some big names in the industry.

Friendship ended with tech, now small cap value is my best friend

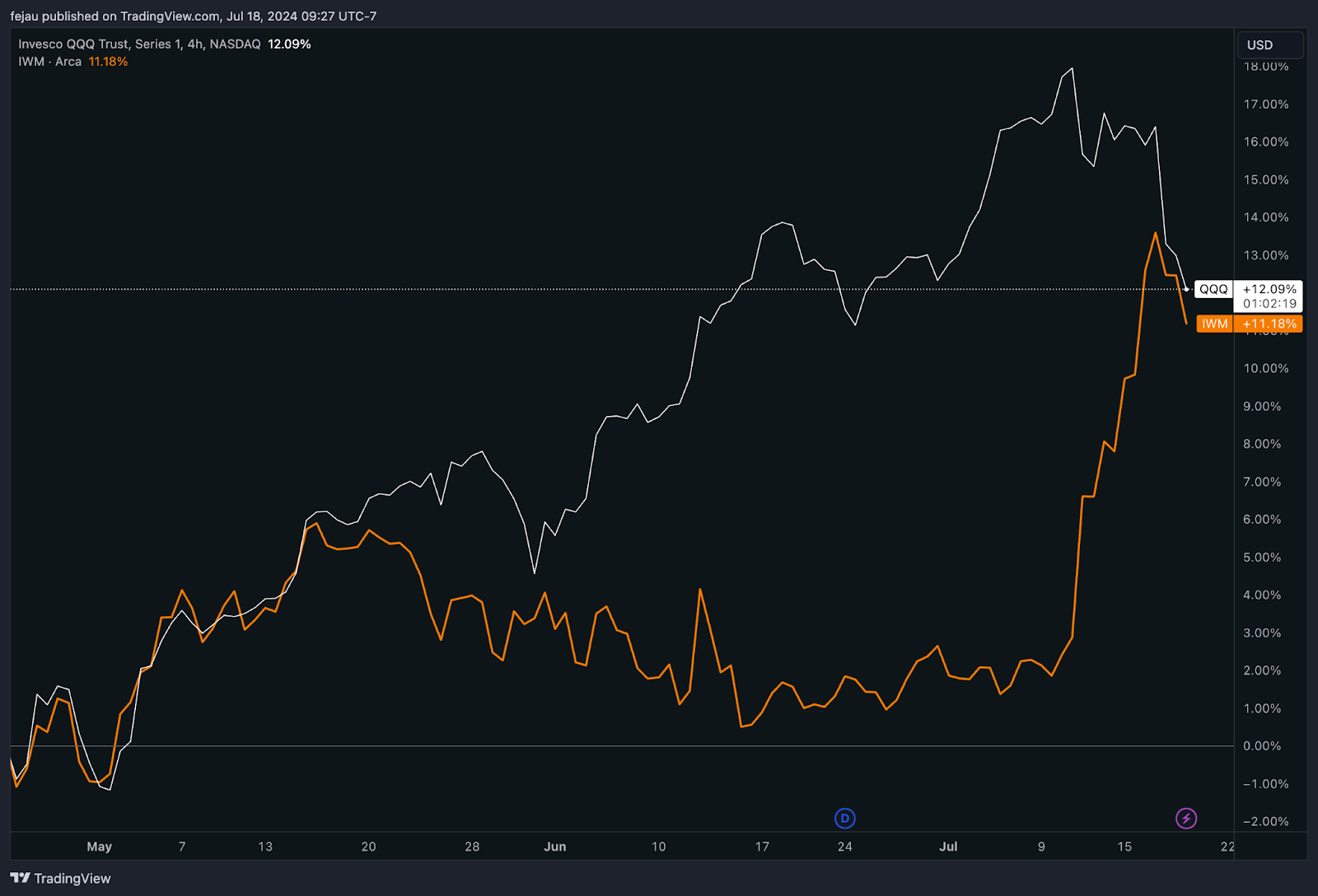

Ever since the ice-cold June CPI print, a major rotation has been underway from large cap tech behemoths (observed via the QQQ ETF) into small cap value-tilted stocks (observed via IWM ETF).

This recent move has been swift and caught a lot of people off guard, as everyone had been piling into the tech trade driven by the AI boom for months now.

As seen in the chart below, QQQ had dominated performance for months until IWM finally caught up:

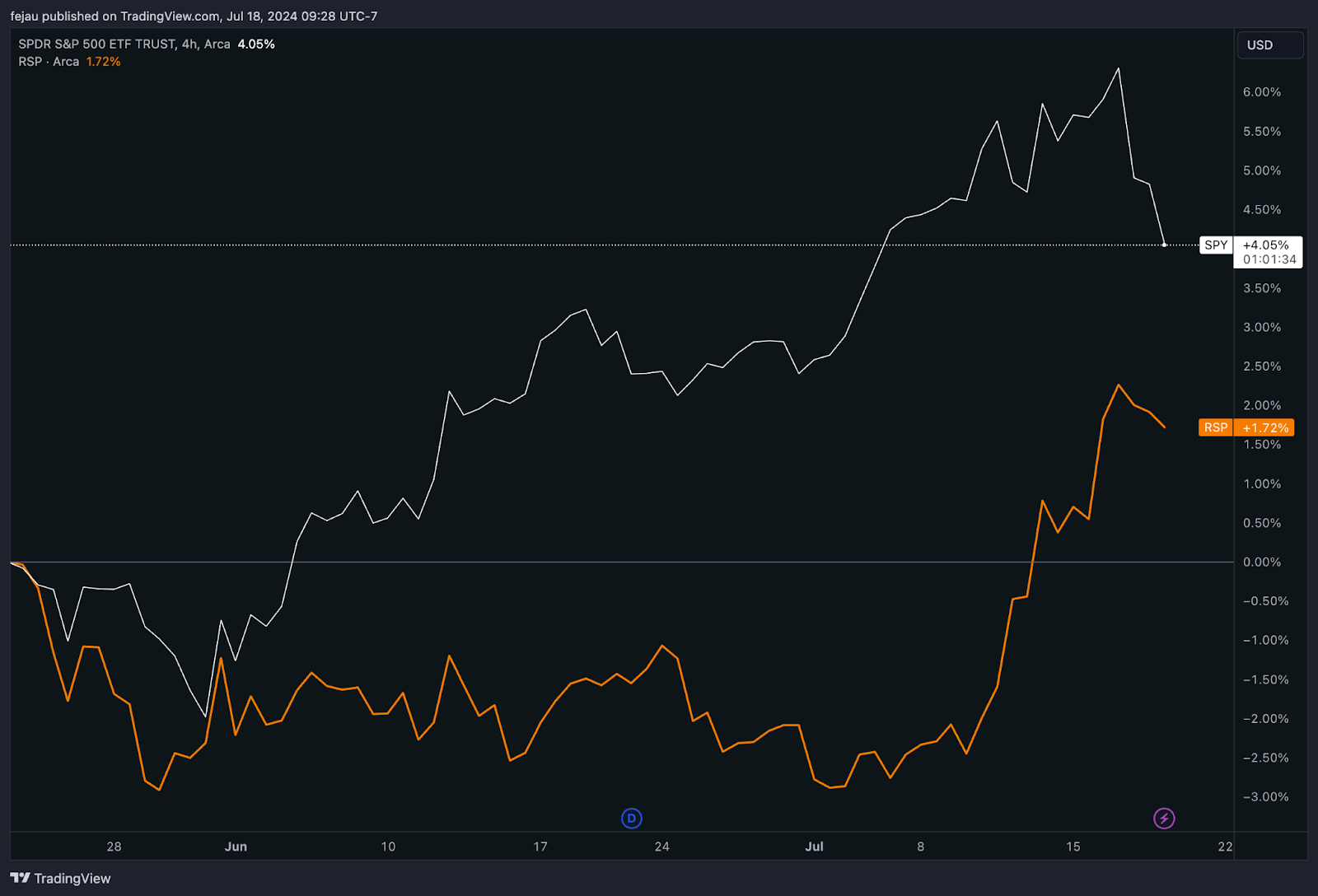

During that same time, SPY (market cap weighted S&P 500) had dominated RSP (equally weighted S&P 500) until it also caught up as of late:

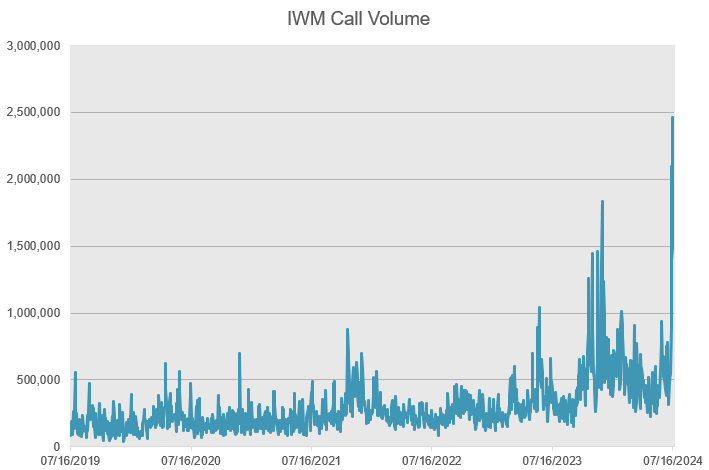

As this rotation accelerated, we’ve seen the classic sign of retail degens piling into a trade: a huge spike in call option volume.

This violent move has left many wondering what caused this rotation to finally happen and what its implications may be. As with anything related to markets, it’s easy to come up with a million reasons to justify a move, and admittedly, it can often just be technical. That said, let’s dig into what I believe is one of the more fundamental reasons why: a lower cost of capital.

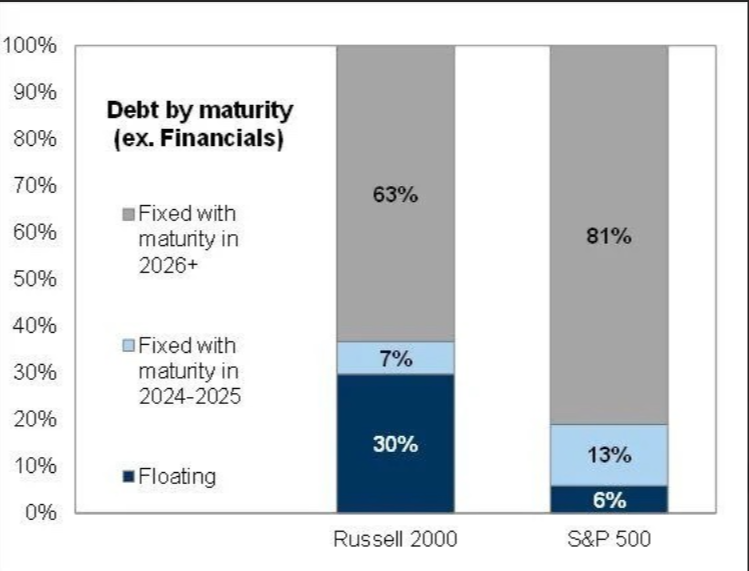

The chart below shows the aggregated debt profile of companies in the Russell 2000 (IWM) and the S&P 500 (SPY):

We can derive a few key insights:

- IWM companies have much more floating rate debt on their balance sheet, which means they are much more sensitive to changes in interest rates.

- The majority of SPY companies have fixed debt that they termed out at very low rates before the rate hiking cycle, which has allowed them to sail this recent tightening cycle relatively unscathed. This is a big reason why so many piled into these names.

- IWM companies generally lean more toward being high yield debt issuers rather than investment grade debt issuers such as those in the SPY. This means the credit risk attached to the debt is larger than that of investment grade corporate issuers.

The key here is that floating rate debt is priced at MRR (market reference rate) plus add-on rate for credit risk. Therefore, if the MRR, which is primarily SOFR (and SOFR is anchored to Fed funds rate), goes down, the cost of debt for these companies goes down, which will generally lead to higher profitability and therefore higher stock price.

Now, let’s circle back to the beginning where I discussed the ice-cold CPI print for June. This has led to the market pricing in a 100% chance of the Fed cutting rates in September for the first time since they began this hiking cycle.

As forward-looking markets begin to price in more FFR cuts, it is natural that investors would rotate into companies with more floating rate debt that will experience tailwinds from a lowered cost of capital.

— Felix Jauvin

ETH ETF fees are in

Competitors in the upcoming US spot ether ETF category have set their planned fees.

The price point is one factor investors consider when choosing a fund to allocate to — with others being its liquidity, the issuer’s brand, etc.

Franklin Templeton’s ETH fund is set to be the cheapest option, for now, at 0.19%.

Grayscale indicated it’s set to keep the fee for its Ethereum Trust (ETHE, as it converts to an ETF) at 2.5%. But the crypto-focused asset manager is set to offer a cheaper “Mini” version of the fund — into which 10% of ether holdings from ETHE will be transferred. ETHE currently manages roughly $10 billion in assets.

A look at the planned US spot ETH ETF fees (excluding initial fee waivers) are below:

| Potential Issuer | Planned ETH ETF Fee |

| Franklin Templeton | 0.19% |

| VanEck | 0.20% |

| Bitwise | 0.20% |

| 21Shares | 0.21% |

| Invesco/Galaxy | 0.25% |

| BlackRock | 0.25% |

| Fidelity | 0.25% |

| Grayscale (Mini) | 0.25% |

| Grayscale (ETHE) | 2.5% |

| ProShares | Not disclosed (as of writing) |

Perhaps notably, Grayscale chose not to undercut its opponents with its Mini Trust fee — a move some industry watchers had forecasted.

Scott Johnsson, general partner at Van Buren Capital, noted in an X post: “Investors selling ETHE are probably not going to be charitable with your mid-price mini option after you stick them with a 10x fee and force them to realize gains.”

“It has a liquidity head start,” he said of the Grayscale offering. “May pay off, but certainly riskier.”

All of these soon-to-be ETH fund issuers, and a couple others, launched spot bitcoin ETFs in January.

Shown below are firms’ spot BTC ETF fees, as well as the net flows (in millions $) each has seen since then, according to Farside Investors data.

| Firm | BTC ETF Fee | Net Flows (millions $) |

| Franklin Templeton | 0.19% | 390 |

| Bitwise | 0.20% | 2,156 |

| VanEck | 0.20% | 583 |

| Ark Invest/21Shares | 0.21% | 2,656 |

| Invesco/Galaxy | 0.25% | 339 |

| BlackRock | 0.25% | 18,750 |

| Fidelity | 0.25% | 9,819 |

| WisdomTree | 0.25% | 70 |

| Valkyrie/CoinShares | 0.25% | 520 |

| Grayscale (GBTC) | 1.5% | -18,692 |

So what does this tell us?

Well, the issuers (aside from Grayscale) decided to offer ETH fund fees that match their bitcoin ETFs.

We can also see that lower fees — particularly when all but one are priced in a similar range — do not necessarily lead to more inflows.

Sources have told Blockworks they expect the US spot ether ETFs to launch on July 23. So we should know soon enough which funds attract the most investor capital out of the gate.

— Ben Strack

Trump campaign ups its USDC holdings

Crypto donors are showing up for Trump, according to the latest campaign finance filings.

Two Trump PACs brought in a combined $3 million in crypto donations, which were converted upon receipt into stablecoin USDC. The Trump campaign has raised a total of $331 million in the second quarter.

The big crypto donors were, as expected, big crypto names.

Cameron and Tyler Winkelvoss gave a combined total of 31 BTC, or roughly $2 million, to the Trump 47 Committee PAC. The donation was given on June 20. The next day, the twins reported that they had been refunded a portion of the donation, which exceeded the individual contribution limit of $844,600.

Kraken co-founder Jesse Powell donated 245 ETH, which equals about $840,000. I guess he got the memo.

There were some regular folk who shelled out, too. One retired woman in California gave the Trump 47 Committee 0.7 BTC, worth around $45,000.

One Department of State employee donated 0.04 BTC, around $2,500. A McDonalds engineer also gave $650 of ETH.

In total, there were around 100 donations made in cryptocurrencies including bitcoin, ether and dogecoin.

Trump’s campaign started accepting crypto donations in May. With his running mate, crypto-friendly Sen. JD Vance, now announced, we’d expect the crypto contributions to continue rolling in during Q3.

— Casey Wagner