Tokenization 101: Capturing the Growth of Asset-Backed Finance via Blockchain-Enabled Opportunities

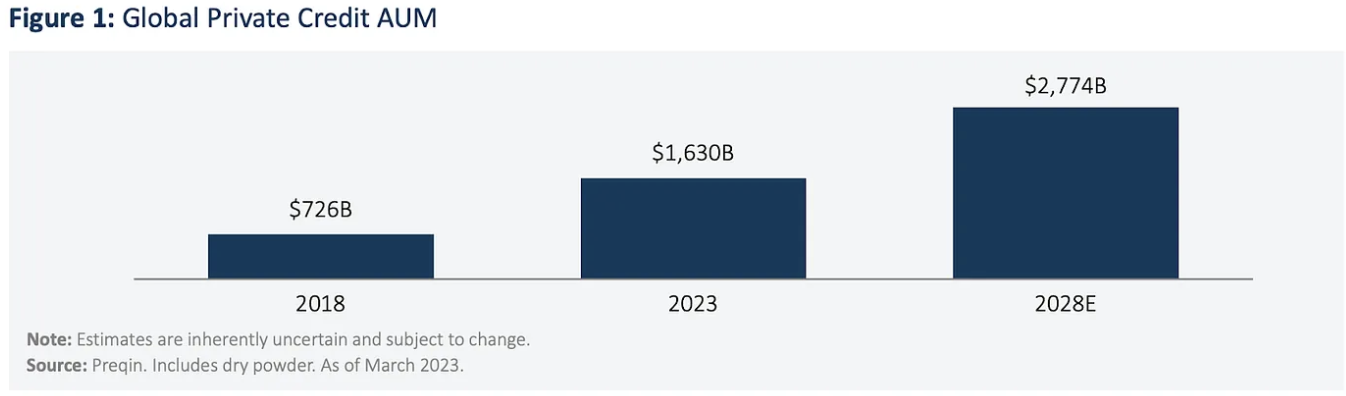

Since the Global Financial Crisis (GFC) in 2008, the growth of the private credit space has been a key theme within the alternative investment management industry. According to TPG Angelo Gordon, private credit strategies grew from $726 billion in global AUM in 2018 to ~$1.6 trillion in 2023. Surveys of market observers and participants suggest that a majority of allocators globally intend to increase or significantly increase their allocations to this space, resulting in an expected $2.8 trillion in private credit assets under management by 2028:

Global Private Credit AUM

To what can this demonstrable growth be attributed?

As a result of the GFC, banks faced increased regulatory requirements and capital constraints, dramatically reducing their lending capacities. This has been especially the case for asset-backed finance (ABF) or specialty credit, which historically has been less standardized and relatively more complex to quantify or capture in terms of data history, ratings, etc.

Outlining ABF

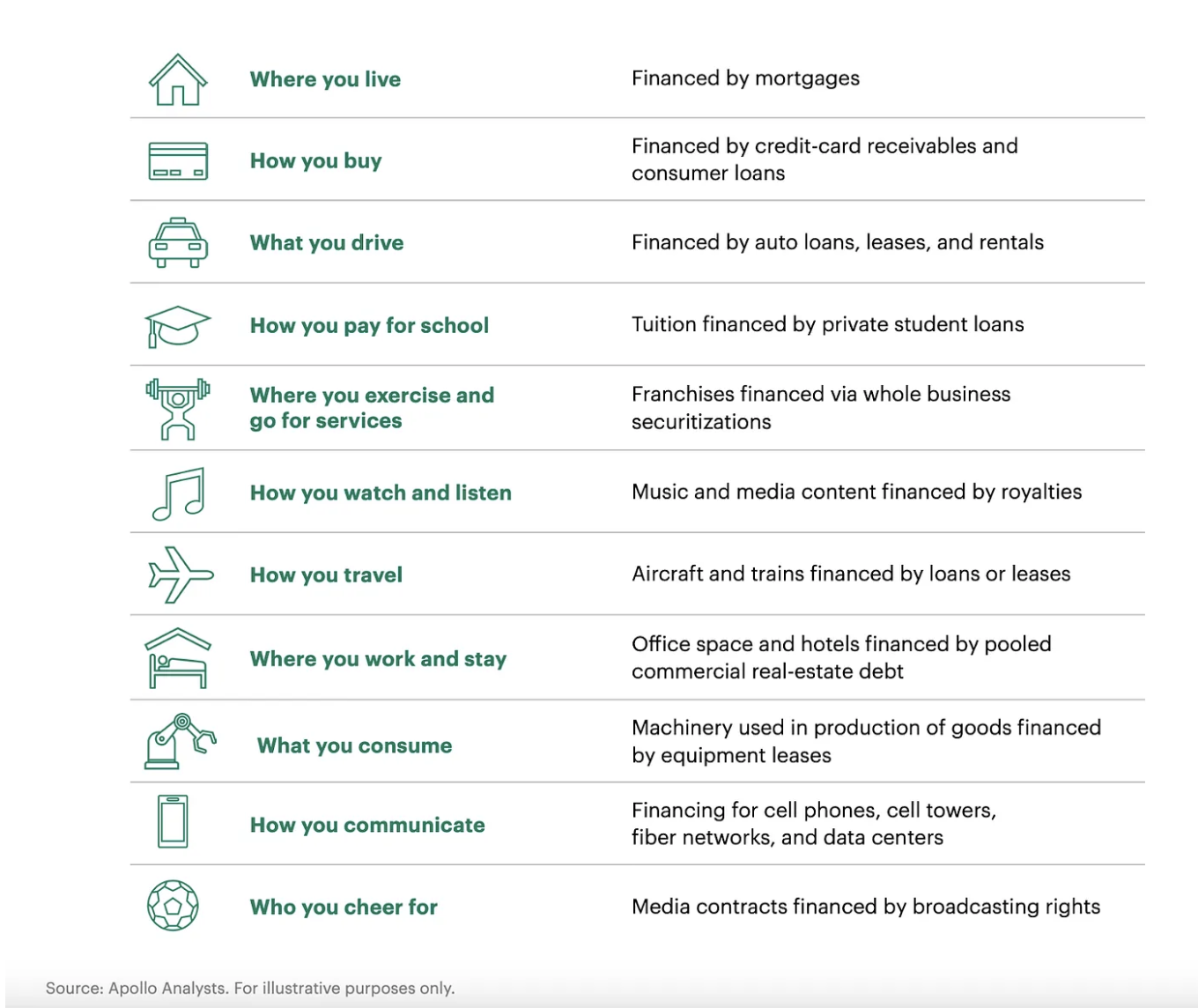

Unlike corporate credit, ABF relies on more than just the full faith and credit of a borrowing enterprise for repayment. Apollo Global Management (“Apollo”) defines ABF as “lending in which a loan is supported first by the contractual cash flows of a pool of assets owned by a limited-purpose borrower, and then by the liquidation of those assets themselves.” To that end, the ABF market is significantly larger than the corporate credit market and includes a whole host of credit types, including those outlined below:

ABF hides in plain sight.

While the contraction in bank lending activity was one of the direct results of the GFC, eroded trust in the traditional banking system was another. At the same time, technological advances in mobile technology and cloud computing, increased venture capital funding, and the utilization of artificial intelligence (AI) and machine learning (ML) to evaluate alternative data collectively led to a rise in financial technology (FinTech) companies disrupting a variety of lending markets. From LendingClub to SoFi, Upstart to Credible, several successful FinTech firms have emerged over the past decade, which, in turn, have helped fuel the growth of ABF and other private credit opportunities.

Among the various ways ABF can be accessed, Apollo describes ownership and control of originators as one of the key ways:

Owning and controlling originators of ABF assets are powerful methods to gain exposure to ABF via direct access to proprietary deal flow. Participants accessing the market in this manner can also gain rights of first refusal on originated loans or leases, as well as rights of first refusal on securitization debt, all while participating in the growth of the platform originator. This access point allows for potentially higher investment spread, given the ability to go directly to the underlying borrower, which reduces the involvement of intermediaries. Like private asset-backed lending, combining structuring expertise and breadth of asset knowledge enables an originator to design a flexible, risk-mitigated credit box. This further allows for the potential to cross-sell and repeat existing business and further drive lower potential risk, given the ability to perform direct due diligence and maintain control of the credit documentation.

Through a combination of equity and debt financing, several alternative asset managers today leverage this model to grow and scale ABF originators while gaining exposure to the space.

Ultimately, as non-bank lenders and specialty finance companies have grown in both number and size, they’ve been not only addressing the funding gap left by traditional bank lenders post-GFC (and further exacerbated by recent bank failures and a ‘higher for longer’ rate environment) but also leveraging their favorable asset-liability mix, structuring expertise and technological capabilities to expand into new and novel assets and markets historically underserved by the traditional banking system.

Blockchain Innovation & Opportunities in ABF

Among the technological innovations and advancements of recent years, blockchain, smart contracts, and tokenization have emerged as tools to further capture the ABF addressable market.

“My ‘aha’ moment in appreciating the revolutionary capabilities of blockchain-, smart-contract, and tokenization-enabled businesses came from an article written by BlockTower Credit Head Kevin Miao,” said Morgan Krupetsky, Senior Director of BD Institutions and Capital Markets at Ava Labs. “In it, Kevin states that these technologies can be leveraged to bypass the many unnecessary third-party service providers that overburden the traditional $14T securitization market and, therefore, achieve a lower capital cost for borrowers. Whether lowering the cost of capital or systemically enabling access to credit across various industries, this upgraded technology stack and the various companies building upon it warrant the attention of today’s ABF investors and capital providers.”

One such example is Intain–a structured finance company whose platform has processed billions in loans through its on-chain administration platform. Combining the benefits of on-chain administration and tokenization, Intain aims to facilitate efficient, cost-effective, and transparent end-to-end asset issuance, investment, administration, and trading. The company strives to dramatically improve the investor and issuer experience by bringing all stakeholders to a shared accountability platform that promotes a single source of truth by providing transparency, continued reconciliation, and an immutable audit trail.

On the investor side, the underlying blockchain technology can improve the experience by delivering real-time transparency into every single loan backing an investment and the ability to collect returns on a more timely basis. On the issuer side, using automated smart contracts reduces the cost of issuance by 50–100 basis points on average. The platform enables an 80% reduction in the days it takes to validate a loan pool, a 65% reduction in the days it takes to underwrite a deal, and a 90% reduction in the days it takes to complete post-closing administration.

Looking Ahead

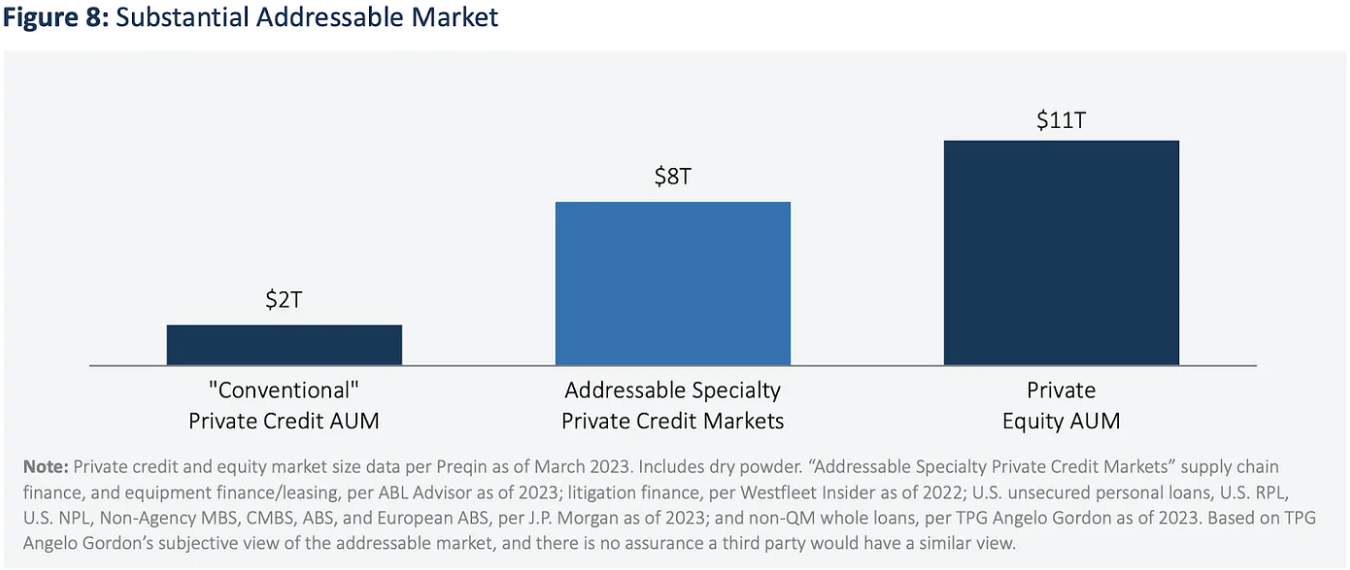

The current addressable specialty private credit markets stand at $8 trillion.

Substantial Addressable Market

Many of the originators building on blockchain today–across home equity, reinsurance, receivables, commercial real estate, and media/IP rights, to name a few–bring to bear their industry expertise and embedded networks. They understand acutely the industry pain points for which they are solving. They are building blockchain-enabled businesses and creating value propositions that either do not exist or are substantially more expensive via traditional transaction, settlement, and administration rails (because of economic or operational infeasibility). As these companies source debt financing facilities to scale, many of them stand to benefit from alternative asset managers’ structuring expertise and the ability to grow alongside strategic equity partners. This combination of debt and equity exposure (plus the added benefit of potential liquid token upside) can potentially provide a compelling return opportunity for investors.

About Avalanche

Avalanche is a smart contracts platform that scales infinitely and regularly finalizes transactions in less than one second. Its novel consensus protocol, Subnet infrastructure, and HyperSDK toolkit enable Web3 developers to easily launch powerful, custom blockchain solutions. Build anything you want, any way you want, on the eco-friendly blockchain designed for Web3 devs.